Search

Please Share your Email if you Wish to Receive the Golden Tips & Tales Newsletter from History of Ceylon Tea Website

I have read with interest the article ‘The Evolution of Sri Lanka’s Plantation Sector’, written by my good friend Sunil Poholiyadde, which appeared in the Financial Section of the Ceylon Today Newspaper on Sunday, 5 August 2018. It is not clear to me whether Poholiyadde has written this article as an ex-planter, the Managing Director of Richard Peries Plantations or as Chairman of the Planters’ Association of Ceylon.

Poholiyadde and I were both Superintendents at the time of the 1st stage of privatization of plantations. He was a reputed rubber planter with the Janatha Estates Development Board (JEDB) and the writer, a tea planter with the Sri Lanka State Plantations Corporation (SLSPC).

Let me at the outset elaborate on the manner in which the privatization of plantations took place for the edification of readers.

The Government at the time considered that plantations should be privatized to bring in ‘private sector management styles and dynamism’ as well as to relieve themselves of the burden of managing plantations. Thus, 22 State-owned Regional Plantation Companies [RPCs] were carved out by the Plantations Restructuring Unit (PRU). Following competitive bidding by interested companies, the management of these State-owned RPCs was handed over in June 1992, to the successful bidders (Managing Agents), for a period of five years.

Some estates of both the SLSPC and JEDB in the Matale and Kandy districts, which were then considered unviable, were retained by these organizations and not included amongst the estates allocated to any RPC. These State-owned RPCs were handed over to the Managing Agent’s ‘debt free’ and working capital requirements were to be obtained from banks by the Managing Agents on behalf of the RPC they were assigned to manage.

With the Government’s decision to divest 51% of the shares of these State-owned RPCs, the initial RPCs to be so divested were the RPCs which had recorded profits during the period they were privately managed.

The 51% of the shares of these ‘profit making’ RPCs were offered to the Managing Agents at the par value of Rs 10 per share,thereby resulting in these Managing Agent’s purchasing 51% of the shares of each of the RPCs for a mere Rs 102 million!

The purchase of 51% of the shares in the RPC also entitled the Managing Agent to the ‘Leasehold Rights’ of the RPC for a period of 53 years. The only criterion in offering these RPCs on this basis was ‘profits’ and with no consideration being given as to whether such ‘profits’ had been derived through the reduction of inputs, stripping of assets, market conditions that prevailed, etc.

As for the RPCs that had not recorded profits during the period they were privately managed, 51% of the shares of these RPCs, as well as their ‘Leasehold Rights’ were offered on the stock exchange for a period of 53 years. These shares sold for sums well in excess of the par value of Rs 10 with one even going up to around Rs 70 a share. The only RPC which was not ‘profit making’ where its shares sold at the par value when offered on the stock exchange was Madulsima Plantations Limited.

Therefore, it would be evident that the ‘non-profit making’ RPCs sold at much higher prices per share than the ‘profit making’ RPCs.

As far as I can recall, the seven (7) ‘profit-making’ RPCs were Agalawatte Plantations, Bogowantalawa Plantations, Horana Plantations, Kegalle Plantations, Kelani Valley Plantations, Kotagala Plantations and Talawakelle Plantations. 51% of the shares (which were 10,200,000 shares) of each of these RPCs were sold at the par value of Rs 10 with the total income realized by the Government for the seven (7) RPCs being Rs 714,000,000.

With the ‘non-profit making’ RPCs selling at an average of around Rs 25 per share, it would be obvious that if the ‘profit-making’ RPCs too were offered for sale on the stock exchange, they too would have realized a minimum of Rs 25 per share, whereby each ‘profit making’ RPC would have realized Rs 255,000,000 and for the seven (7) profit making RPCs a total of Rs 1,785,000.

The resultant loss to the Government, in the flawed and ad hoc process by which the controlling interest of ‘profit-making’ RPCs were sold, resulted in a loss of over Rs 1 billion on the sale of the ‘profit-making’ RPCs. With many alleged misdemeanors of the past being investigated, this loss of revenue to the State too should be investigated.

Therefore, while it is an undisputed fact that the controlling interest of ‘profit-making’ RPCs were sold at a pittance, the controlling interest of the ‘non-profit making’ RPCs were sold following competitive bidding, by interested parties, on the Colombo Stock Exchange. Further, it would be evident that the controlling interest of all RPCs was bought by buyers who were well aware of all factors applicable to/prevalent in the RPC.

The land on the estates of each RPC belonged to the SLSPC and JEDB. Accordingly, the Indentures of Lease, entered into in respect of each individual estate of each RPC, were signed on behalf of the SLSPC/JEDB by its Chairman and another Director based on which organization owned and had managed the respective estate previously.

The purchaser of the controlling interest of each RPC was permitted, in the Indentures of Lease, to raise finances by mortgaging the land of the RPC, despite the fact that the land continued to belong to the SLSPC or JEDB.

However, the concession of doing so was not permitted to either the SLSPC or JEDB, in respect of the estates which remained with them, despite them being owners of land!

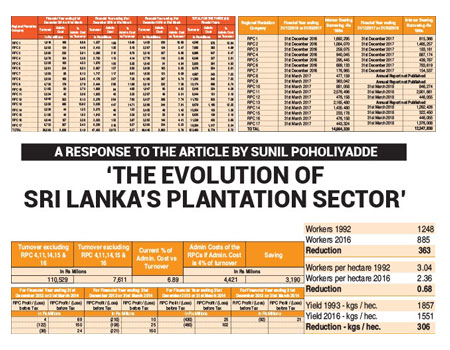

Another benefit afforded to the Managing Agents was the option for them to recruit personnel they wished to as well as ‘second’ any personnel to the RPC from the ‘parent company’. I give below a statement indicating the Administration Costs and Turnovers of RPCs over three Financial Years where the Administration Cost of each RPC has been shown as a % on their turnover.

On perusal of this statement, it would be noted that the Administration Costs of RPCs on a percentage of their turnover over three (3) Financial Years, varies from a low of 1.30% in RPC 14 to a high of 12.64% in RPC 1. This does not appear to be justifiable as the RPCs are all with similar extents and in any event not so incomparable in extent that they would have such a wide variance in Administration Costs. It would also be noted that five (5) RPCs - RPC 4, RPC 11, RPC 14, RPC 15 and RPC 16 – have Administration Costs which are less than 4% of their turnover.

From the above it is evident that if some RPCs can have their Administration Costs at less than 4% of their turnover, it is obviously an indication that the others too can do likewise. Hence, one wonders whether there has been abuse of this privilege by the RPCs.

Further, if the RPCs which have an Administration Cost in excess of 4% of their turnover, reduce their Administration Cost to 4% of their turnover, the saving on Administration Costs for the three-year period would be a colossal Rs 3.19 billion; please see relevant details below:

Yet another concession extended to the Managing Agents was that they were entitled to a ‘Management Fee’ for managing the RPCs. These Managing Agents were entitled to this ‘Management Fee’ irrespective of whether the RPC recorded a profit or loss. It must be stated that some Managing Agents have unethically (not illegally) drawn out vast sums of money from the RPCs, despite the RPC itself recording a significant loss, while others have not done so thereby showing their commitment in the management of their RPCs.

Examples of some of the unethical (not illegal) Management Fees drawn when the RPC itself has recorded a loss or made a minimal profit are given below; I cannot agree in any way with Poholiyadde’s statement “By the time privatization was completed in 1992, conditions on the estates had reached their lowest point” as it is an undisputed fact that estates both in the SLSPC and JEDB were in prime agricultural condition.

This statement in addition to being incorrect is a slur not only on the ability of all planting executives including Poholiyadde and the CEOs of RPCs who were planting executives of estates of the SLSPC or JEDB prior to privatization, but also on J. R. Jayewardena, Gamini Dissanayake, Ranjan Wijeratne, Rupa Karunatilleke who were the Ministers under whose purview the SLSPC and JEDB functioned as well Kenneth Ratwatte, Denham de Alwis, Ranjan Wijeratne, Jayasiri Perera, Malcolm Peries and Nihal Illangakoon all of who were Chairmen of the SLSPC and Pemsith Seneviratne and Lincoln Perera who were Chairmen of the JEDB.

If, in fact, there is an iota of truth in the statement on the “inability of the State to manage the plantations”, I doubt Sri Lanka would have achieved in 1991, its highest ever tea crop of 224 million tonnes, with the estates of SLSPC and JEDB contributing almost 65% of this crop!

It would also be pertinent to state that the total tea production prior to 1992 was around 65% being from the SLSPC and JEDB estates with the balance being from smallholders.

This scenario has diametrically changed and presently the production by RPCs (which comprise the estates previously with the SLSPC and JEDB) is around 30% while smallholder production is 70% of Sri Lanka’s total tea crop!

The article also boasts of the Tea Yield per Hectare having increased to 1,138 kg/ha in 2016 from 1,021 kg/ha in 1992. This represents an increase of a mere 11% over a period of 24 years and is far from being significant or even worthy of mention.

There were large extents of re-plantings, which had yet to be brought to maturity at the time of privatization and with these coming into the production, an increase of just over 11% in Yield per Hectare, over 24 years, is dismal.

Reference has also been made regarding cadres on estates with that stated being “while the numbers employed in these estates ballooned in size with the country’s political class increasingly viewing the sector as a job bank to purchase support each election cycle”.

On SLSPC estates when Ranjan Wijeratne was Chairman, he personally visited every estate and in consultation with the Regional Board Chairman, the Regional Director and the Estate Superintendent, drew up a forward development programme which included replanting, infilling of vacancies, factory development, improvement to worker housing and other worker amenities, improvement to staff and executive housing, vehicle requirements, etc. Based on these forward programmes, staff and worker cadres, including increases necessary in future years to meet the planned development, were determined and these cadres were not exceeded under any circumstances.

I am personally unaware of whether a similar exercise was done for JEDB estates but have no reason to believe that it was not done.

When RPCs took over the management of estates and with their intention to curtail work (including replanting, infilling and other basic agricultural practices such as draining, forking, etc.) to reduce costs, they obviously found worker cadres excessive.

The cadre existent on estates was based on the actual requirement of work to be done and became excessive only with the curtailment of work described above. Therefore, RPCs did not recruit any youth seeking employment and retired all workers reaching the age of retirement.

This led to the outmigration of youth on estate to the cities and towns where they found employment and though the employment they found was menial, it enabled them to return to the estates especially during festivals, smartly clad and having money, which encouraged others to follow suit.

Therefore, this exodus of workers, was created by the RPCs themselves and has resulted in estates presently being severely short of workers to even attend to accepted practices such as plucking (harvesting) on a duration depending on elevation.

This exodus of workers has also resulted in some RPCs abandoning productive extents of both mature Tea and Rubber. A clear example would be what is seen when driving up to Hatton from Ginigathena!

An example of the reduction of workers and what it has resulted in is given below, based on the ‘actuals’ on an RPC estate in the Hatton District;

While the large amounts of Rubber having being replanted are referred to, there is no mention of any significant replanting of tea.

As for Rubber, with prices being poor, as has been the case for many years, it is obvious that no proper forecast on future market conditions was done prior to undertaking the replanting of these large extents of Rubber.

Further, with the replanting costs of Rubber being virtually covered by the income derived on the sale of the old existing Rubber, this too should be considered when the large-scale replanting of Rubber is referred to. In fact, some RPCs have even sold the existing Rubber trees but not undertaken replanting leaving these extents idle.

With the claim that RPCs have increased Rubber yields from 647 kgs/ha in 1992 to 862 kgs/ha in 2016, this is actually only a 33 % increase over a period of 24 years! Further, with the claim that large amounts of replanting claimed, this increase too, as in the case of Tea, is hardly worth mention and, in fact, dismal!

With regard to replanting of Tea, the reason given by Managing Agents of RPCs is that the ‘return on investment’ does not justify such work being done.

This is a senseless and totally unacceptable excuse trotted out by most RPCs. If Infilling [re-placing of dead tea bushes] and re-planting is not carried out how on earth can one expect to increase productivity?

If this claim of ‘re-planting and lack of return of investment’ is correct, the contention of the Managing Agent’s may have been justified if funds for this work were being made available by the majority shareholder on the premise that he may not have been able to recover his investment within the stipulated lease period.

However, with the majority shareholder having the ability of obtaining financing by mortgaging the assets of the RPC, which has been done liberally, the contention of the Managing Agent is unacceptable. A salient point which appears to have been missed or disregarded is that if replanting or any other capital development is undertaken, the asset value of not only the estate but also the RPC increases.

Poholiyadde’s article also refers to the SLSPC and JEDB requiring to be funded to the tune of Rs 400 million a month to ensure their existence. I find this impossible to accept, unless of course such funding was required, if at all, in 1992 when Sri Lanka experienced probably its worst ever drought. To substantiate my contention – the SLSPC had estates in the Regions of Nuwara Eliya, Haputale, Hatton, Ratnapura, Galle/Matara, Kalutara and Matale/Kandy of which, other than for the Matale/Kandy Region, all other Regions were profitable.

Similarly, of the JEDB Regions – Nuwara Eliya, Badulla, Hatton, Avissawella, Kurunegala, Chilaw and Kandy, to the best of my knowledge, it was only the Kandy Region which was running at a loss. It would also be necessary to mention that the reason for the SLSPC’s Matale Region and the JEDB’s Kandy Region to run at a loss was due to estates in these regions being those, both the SLSPC and JEDB, inherited from the Usawasama and Janawasa’s around 1978.

The article also refers to the State-managed estates currently under the purview of the SLSPC and JEDB. These estates are all in the Kandy/Matale districts and were those which, after nationalization in 1972, were under the purview of the Usawasama and Janawasa until around 1978 when they were brought under the control of the JEDB and SLSPC. These estates had been considerably neglected during the period they were under the purview of the Usawasama and Janawasa, and despite much effort being put in, after they were brought under the purview of the JEDB and SLSPC, at the time of privatization, they were not considered suitable to be included amongst the RPCs. This alone shows that only the better estates of the SLSPC and JEDB were privatized.

Another, ‘benefit’ which accrued to the RPCs was that all proceeds on the sale of produce awaiting sale both with the Brokers or in stock on the estates (which was around six weeks production) at the time of the incorporation of the RPCs, were remitted to the RPCs and not the SLSPC or JEDB who had borne the cost of such produce being manufactured.

In fact, if the SLSPC and JEDB were able to obtain financing on the same basis as done by the RPCs, I am quite certain that these estates would have shown considerable progress, even exceeding that of some RPCs.

As regards the non-payment of statutory dues by the SLSPC and JEDB, this is not condoned. However, one must appreciate that it was obviously due to a serious lack of working capital.

With the infusion of funds by the Treasury, I am made to understand that most of these outstanding statutory dues have been settled. Despite all the facilities of obtaining easy finance available to RPCs, there are some among them too who have defaulted in making such payments as well as lease rentals payable to the State.

Therefore, the comparison of the estates currently with the SLSPC and JEDB with estates of the RPCs is similar to comparing ‘chalk and cheese’ and is therefore irrational.

With the facility available to the majority shareholder in mortgaging the assets of the RPC to raise financing, the financing obtained by the 17 RPCs listed on the Colombo Stock Exchange are given in the statement below with the details extracted for their last completed Annual Reports:

Poholiyadde also states that Rs 70 billion has been invested by the RPCs. Of this amount, it would be interesting to know;

a) How much of this was cash infused by the majority shareholder of the RPCs,

b) How much was by way of grants received for worker housing and provision of other worker amenities,

c) How much was funding from the World Bank, ADB, etc.,

d) How much was generated on mortgaging the assets of the RPC, and

e) How much of (a), (b), (c) and (d) was actually invested on the development of estates in the RPC.

I find it amusing to read the reasons given for the reduction in RPC tea production which are “Severe encroachments, a shrinking labour force and the periodical obstacles created by Government policy interventions”.

My observation of the reasons given is as follows:

In fact, if such lame excuses had been given to industry legends such as Ranjan Wijeratne, those doing so would have not been on the estate they were on to see the sun rising the next day.

The present Government, obviously realizing that shortcomings are prevalent in the management of RPCs, created what is referred to as the Plantations Reforms Committee. Though this Committee had arranged for both an Agricultural Audit to be done on some estates of each RPC and a Financial Audit done on each RPC itself, the reports of these audits have yet to be publicized. Therefore, it is my fervent wish that these reports will be made available to the people of Sri Lanka very early as they are entitled to being aware of the contents of these reports as it is, in fact, their assets which are being managed by the RPCs.

This response to Poholiyadde’s article is done without fear or favour and with malice to none, with my only wish being that the RPCs would correct the shortcomings on their part and bring the plantation industry back to its glory. In fact, this is probably the only instance where the private sector, renowned for its dynamism, has failed despite the significant concessions made available to them to facilitate their successful and effective management of the plantations.

Devaka Wickramasuriya

The writer was a Planter and a Superintendent with the SLSPC in 1992 at the time of the initial stage of privatization. He was also at that time Deputy President of the Ceylon Planters Society and was actively involved in the identification and resolution of issues planters, of both the SLSPC and JEDB, could have faced after privatization. He also served as General Manager – Plantations of Carsons Agro Services Limited, a company that was selected to manage plantations in the 1st stage of privatization. His last post in the plantation industry was as Chairman of Elkaduwa Plantations Limited, a State-owned and managed Regional Plantation Company. He could be contacted on devakaw@sltnet.lk.

Source - www.ceylontoday.lk/print-edition/2/print-more/10689

Comments

(In keeping with the objectives of this website, all COMMENTS must be made in the spirit of contributing to the history of this estate, planter or person i.e. names, dates & anecdotes. Critical evaluations or adverse comments of any sort are not acceptable and will be deleted without notice – read full Comments Policy here)